If you are claiming R&D tax relief, it’s important to understand the correspondence you might receive from HMRC and what to do next. Before late 2022, most applications for R&D tax relief resulted in money hitting your bank account, with little or no direct communication between you and HMRC. But times have changed.

As we discuss in our R&D fraud, error and non-compliance overview, HMRC has changed its approach to R&D claims in recent years in an attempt to prevent misuse. The extension of the Individuals and Small Business Compliance (ISBC) team’s remit to include R&D compliance in late 2022, as part of HMRC’s Campaigns & Projects team, has significantly shifted the compliance landscape. As a result, compliance checks are now increasingly common.

So, what do HMRC R&D letters look like? What do they ask for? And, importantly, what do you need to do?

HMRC correspondence: R&D tax

There are a range of compliance tools available to HMRC and the correspondence relating to each looks slightly different. Deciphering that correspondence isn’t always simple, so we’ll look at the types of correspondence you might receive, along with the terminology.

Before getting started, here’s a summary of what you need to know:

- Take any HMRC letter about your R&D claim seriously.

- Payment doesn’t equal approval – just because you’ve received payment doesn’t mean that HMRC has approved your R&D claim. They have processed it, but they may subsequently check that the claim is correct.

- R&D tax advice is a (largely) unregulated market and one that has attracted spurious advisers. You therefore may be exposed to potential risks without knowing it.

- Remember that you carry the risk associated with your R&D claim, not your adviser or accountant.

- HMRC’s increased compliance activity has resulted in enquiries rising significantly.

HMRC R&D compliance letter

When you submit an R&D tax relief claim to HMRC, it should typically be processed by HMRC within 40 days. On occasion, HMRC will ask for more information to clarify questions. This process is known as an ‘enquiry’, and it can be raised before or after your claim has been processed.

If you’ve received a letter from HMRC stating that it is conducting a compliance check into your R&D tax credit claim, this is typically the start of the enquiry. There are exceptions, such as ERIS checks, where HMRC has sent letters requiring you to take action, which are outside the formal enquiry framework but must be responded to.

Compliance check letters may be sent by one of three teams:

- Large Business (LB) Compliance

- Wealthy and Mid-Sized Business Compliance (WMBC), or

- Individuals and Small Business Compliance (ISBC).

Each team operates slightly differently, but it is vital that you take them seriously, and act quickly.

What is an R&D tax relief compliance letter?

An R&D tax relief compliance letter is HMRC’s way of communicating with you that they need more information about your R&D claim to check if the submission has been made correctly.

It is important to remember that compliance checks can look at your whole company tax return, so they can be quite broad in scope. The opening letter will define the scope of HMRC’s compliance check; if it includes your R&D claim, it will say just that.

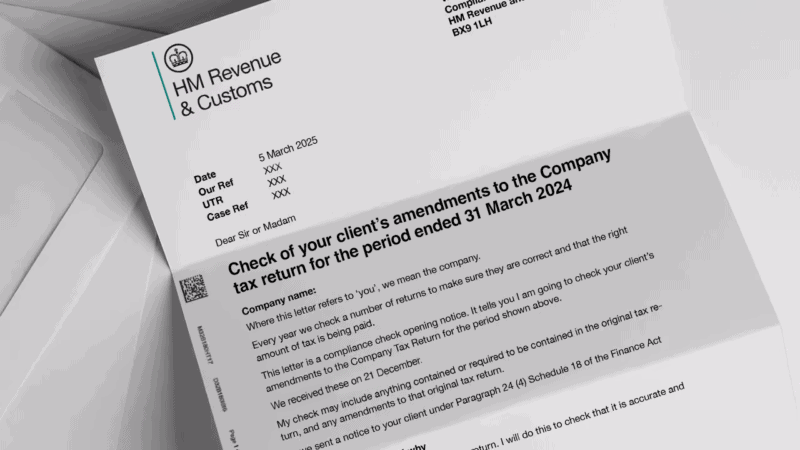

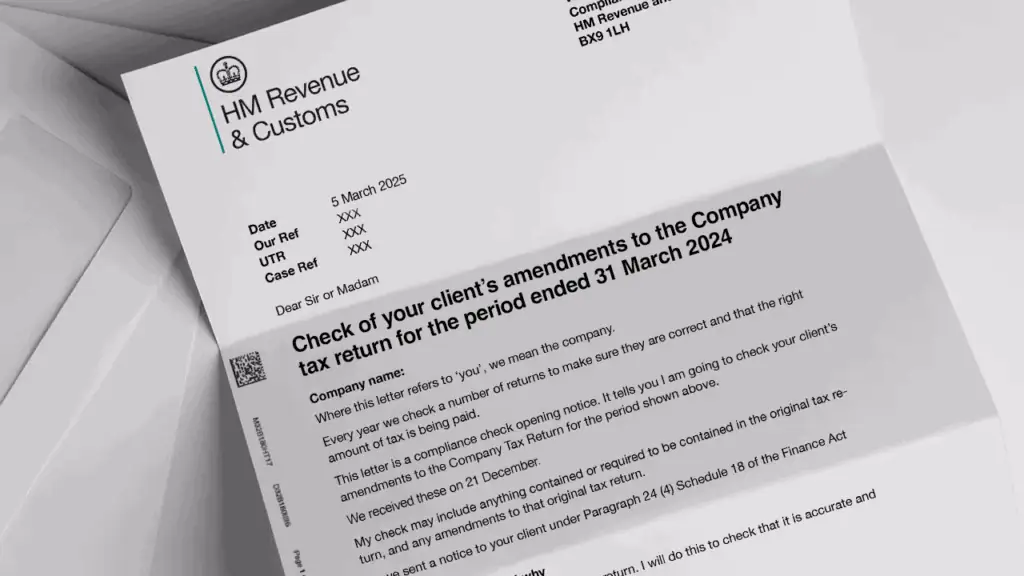

Identifying a compliance check letter

The letter will explain that it is a compliance check opening notice. In the same way HMRC usually refers to taxpayers as ‘customers’, an enquiry letter rarely includes the word ‘enquiry’ in it. Instead, you’ll receive a letter titled:

“Check of the Company tax return for the period ended…”

The correspondence will state the legislative provisions which HMRC are using to open the compliance check and should include a number of enclosures. The enclosures should include several factsheets to help you understand your rights as a taxpayer and how to correspond with HMRC. A common factsheet to be included is the CC/FS1a ‘About compliance checks’.

An opening letter can run to nine or ten pages and it is important to identify the specific questions within this opening letter which you need to address. The letter will almost always provide a deadline by which HMRC want you to respond.

Example R&D compliance check letter

If your letter appears to be a compliance check, but does not mention one explicitly, it may also be one of three types of letters described in our blog on the 2026 compliance landscape. If the letter provides a deadline to respond, you must treat this with the same importance as a formal compliance check.

Why have I received a compliance check letter?

HMRC will open enquiries into a proportion of all R&D tax credit claims. Due to a shift in approach, this proportion has increased. The reasons why HMRC might open an enquiry can vary. It might be related to your company and its status or the nature of your R&D. It might also be unrelated to business type and the company has instead been selected via a sampling approach from HMRC.

The following are some of the more common reasons behind an HMRC enquiry:

- HMRC is focusing enquiries on a particular sector or type of technology to ensure that it is approaching claims in the sector consistently. For example, businesses with certain Standard Industry Classification (SIC) codes, may be at higher risk of an enquiry from ISBC.

- Your business has been selected through HMRC’s current sampling approach.

- HMRC believes it has found an inconsistency – an aspect or detail that it believes requires further review to confirm that the claim is correct. This should be highlighted in its opening letter.

- HMRC is fact-finding following a change in your circumstances, such as an increased claim value, or change in eligibility for the ERIS incentive.

- HMRC has questions about your tax return – which, although unrelated to R&D – has triggered the enquiry. R&D is usually then included for completeness.

What you need to do

The letter is the start of an HMRC enquiry and the most important thing at this point is to treat the matter with urgency. It can be tempting to delay putting a plan in place around your response. Sometimes the importance of the letter, the actions you need to take and the deadline can be lost in the many pages of jargon and guidance.

In short, if you’re facing an enquiry, do not ignore it. You’ll typically have 30 days to respond to the questions or requests in the letter. Always make sure you check the date as the letter will have taken a few days to reach you if it has come by post and the deadline will be based on the date the letter was written. If this feels like a long time, it isn’t. You’ll ideally want your first response to be timely and thorough to avoid a last minute rush.

If you’ve worked with an R&D tax adviser to prepare your R&D claim, then share the letter with them immediately. They should quickly provide you with a plan for how they will manage the response.

If any adjustment is required to be made to the claim following the conclusion of the enquiry, HMRC will consider whether any penalty should be due. How much will depend on the approach taken by the company to prepare the claim, as well as how you have behaved during the enquiry. Missed deadlines or lapses in communication could count against you.

Need support with an HMRC R&D tax credit enquiry?

ForrestBrown has a strong track-record of helping businesses who have either prepared the claim themselves or with another adviser, resolve their enquiry.

If you want expert support, get in touch with our enquiry support team, led by James Dudbridge, Director at ForrestBrown. Made up of a former HMRC inspector, qualified chartered tax advisers and accountants, industry-experienced sector specialists and lawyers, we are ideally placed to protect your business.

FIS letters

Increasing numbers of SMEs are receiving so-called FIS letters, sent out by HMRC’s Fraud Investigation Service (FIS). These letters can be quite alarming, but do not necessarily signal the start of an enquiry. They are a request for additional information and documentation to support the legitimacy of your claim.

What are FIS letters?

Since FIS letters are sent by HMRC’s unit responsible for identifying deliberate non-compliance and tax evasion, they take a serious tone, alleging fraud. The letters state:

“The claim triggered an alert on our systems and has caused HMRC to believe that you have fraudulently claimed money to which you are not entitled. Therefore, HMRC has blocked payment of this money.”

Identifying a FIS letter

Beyond the references to fraud, there are a few other key elements to look out for to confirm you have received a FIS letter:

- request for information and documents to be sent to fisresearchclaims@hmrc.gov.uk. This will often include a request to categorise costs under specific sub-headings such as staffing costs and qualifying expenditure on externally provided workers. It will likely also request bank statements showing the expenditure was incurred and offering the company to provide any further information it feels is relevant to support the R&D claim.

- Details on the rules around claiming R&D tax relief.

- A section that states HMRC “reserves the right to open a criminal investigation into any suspected fraud committed against the R&D scheme.”

- A sign-off from the Fraud Investigation Service.

Why did I receive a FIS letter?

Details are thin on the ground, but ultimately, FIS letters are an attempt by HMRC to tackle R&D fraud. This is deliberate and potentially criminal tax evasion. In recent years, HMRC has increased its capacity and methods to investigate non-compliance. It created the Fraud Investigation Service division to investigate claims where fraud is suspected.

What you need to do

Don’t panic if you’ve received a FIS letter, but do act swiftly. If you do not respond by the deadline set out in the letter, FIS will move to reject your claim straight away. FIS does not accept any requests for extensions on providing the required information.

Your immediate steps should be to:

- Respond to FIS by the deadline set out in the letter.

- Start gathering the information and documents requested including consideration of what additional information above and beyond the AIF submission would be valuable to provide.

- Contact ForrestBrown – you can do so via telephone or email to speak to our dedicated enquiry support team. Alternatively, you can find out more about the service.

Once you’ve responded to FIS, they will review the evidence provided and, you can expect one of a few things to happen:

- your R&D tax relief claim is paid out in full – the unit is satisfied with the information and documentation provided and will process payment, or

- an R&D enquiry will be opened – the unit will contact you to state that the case is being referred to the HMRC compliance team (typically WMBC), and they will be in contact with you when a caseworker is allocated and a formal enquiry will follow, or

- your R&D tax relief claim will be rejected – the unit is not satisified with the response and will issue a correction notice. If you disagree with the correction notice, you will need to consider what mechanisms are available to you to challenge the decision, or to reinstate the claim.

Act now

At ForrestBrown, we take complete control of the situation, working closely with you to respond to HMRC. We will review your claim thoroughly as well as any correspondence received. Our expert team take a proactive approach, tailoring our process to your needs to reach a favourable outcome.

- Telephone

- 0117 926 9022

- hello@forrestbrown.co.uk

AIF follow up letter

Following the introduction of the Additional Information Form (AIF) in August 2023, businesses may now receive an AIF follow-up letter. AIF follow-up letters are sent to the responsible officer named in the AIF, not the agent used to prepare the claim. They invite the taxpayer to take a look at the R&D claim and set out next steps prior to filing it in the Company Tax Return.

They are similar to “concern letters” (discussed below) in that they do not state that they are a compliance check or provide a deadline to respond to HMRC by. The difference between them is that each is received at different points in the claim journey. Whereas a concern letter is received after submission of the claim, an AIF follow-up letter is received after submission of the AIF but often before the tax return has been filed.

What is an AIF letter?

The letters invite businesses to check that they are familiar with the next steps in the process and make clear that the company should not proceed with including the R&D expenditure in its Corporation Tax return if, on reflection, it assesses that there was no R&D activity. It points to useful resources such as the R&D Guidelines for Compliance and outlines the sectors that are unlikely to be eligible for R&D tax relief, including pubs and restaurants, care homes and childcare providers.

It also highlights common mistakes to avoid in R&D claims, as well as reminding the taxpayer of their general responsibilities when submitting a claim.

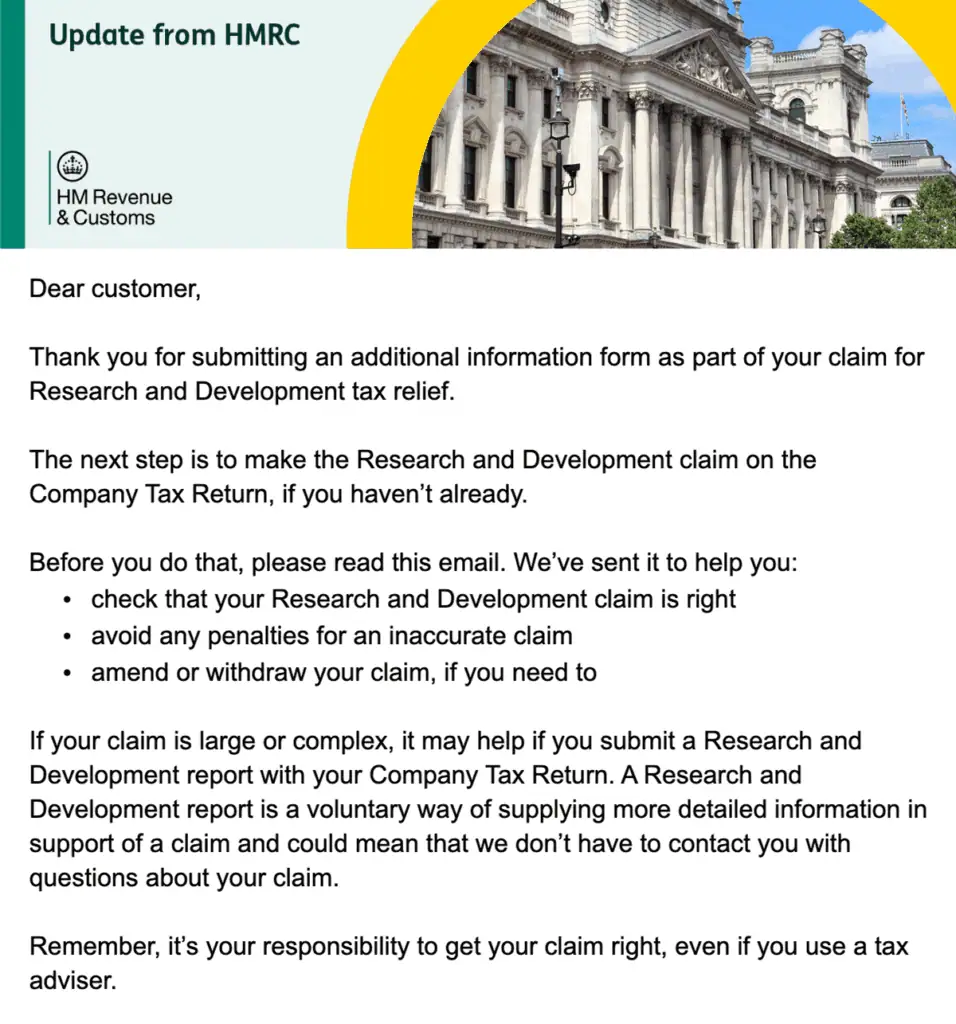

Identifying an AIF letter

AIF letters are informational and often start:

“Thank you for submitting an additional information form as part of your claim for Research & Development tax relief.

The next step is to make the research and development claim on the Company Tax Return…”

They are signed off by “HM Revenue and Customs”, rather than by an individual compliance unit or caseworker.

Why did I receive an AIF letter?

It’s not known what proportion of claimants receive an AIF letter. Since they go directly to the business, an agent might not always know if a claimant has received it. Where they are triggered, it might be for a number of reasons, including random sampling or as a result of the business’s SIC code.

What you need to do

As the AIF letter states, if you are comfortable with your claim you do not need to take any action. Ensure your tax return, including the R&D figures, is submitted before the statutory deadline and wait for confirmation that the claim has been processed. As with all claims, you should keep an eye out for any other correspondence from HMRC regarding your claim such as those explained in this article.

If, on reflection, you believe that you do need to adjust your R&D claim, speak to your adviser or seek a second opinion and review the position. Should it be confirmed that an adjustment is needed, work with your adviser to re-submit the claim prior to the statutory deadline. After the statutory deadline a disclosure would have to be considered. This is where you will need to contact HMRC about the adjustments required, as you will not be able to utilise the gateway for submission.

HMRC R&D eligibility letter

A recent development from HMRC is a form of what may previously have been called a ‘nudge’ letter in the tax world. These new letters are “concern letters”. They invite the company to review its claim and, if it shares HMRC’s concerns about the claim’s validity, to amend its return to withdraw the claim. While we have only seen a handful of these letters, they appear to be an attempt to pre-screen claims for potential future enquiry. Although they are not a compliance check or ‘enquiry’, it does not mean that they can be filed and ignored.

What is an R&D eligibility letter?

Eligibility letters are typically used by HMRC as a proactive way to get companies to address potential errors in their R&D claims. These ‘concern’ letters are likely to feature the phrase: “we’re concerned your company may not be eligible to claim”. The letter will provide high-level reasoning as to why HMRC has a concern regarding eligibility.

Receiving an R&D eligibility letter does not necessarily mean anything is wrong with your R&D claim. That being said, it should absolutely be taken as an opportunity to check that you are fully confident that your claim would withstand a compliance check.

Identifying an eligibility letter

You need to be able to correctly identify an eligibility letter. In our experience, these letters follow a template. You can expect to see the heading: “Your Research and Development (R&D) relief claim”. The most obvious indicator is the continuous use of the word ‘concern’. The letter will include headings such as ‘Your claim may not relate to a qualifying advance’ and ‘Your claim suggests your main trade may not be relevant to {field of science or technology}’ e.g. software. The explanations provided under each heading will reference the requirements for a valid R&D claim and will provide high level connections to the claim that has been submitted. This does not mean HMRC has read your AIF submission in full and may be utilising key sections of the AIF such as the SIC code and field of science or technology to influence the content of the letter.

Why have I received an eligibility letter?

Receiving a ‘concern’ letter does not necessarily mean anything is wrong with your R&D claim. These eligibility check letters are another mechanism for encouraging businesses and their advisers to scrutinise R&D claims and avoid errors. HMRC is under pressure from the National Audit Office to reduce the number of errors in R&D claims that have been uncovered during compliance checks.

By sending out these eligibility letters, HMRC hopes to encourage companies to look at its guidance on R&D claims and check they are comfortable with it. The plan is that companies will review their own claims without the need for an enquiry.

What do I need to do?

What you need to do next depends on whether you have prepared your claim yourself or used an adviser to help you.

I prepared my R&D claim myself – in the correspondence you will see some links to HMRC’s guidance on R&D claims – these resources can be really useful. Ideally you’ll have used these to prepare your claim. If you are not already familiar, you have some reading to do!

If you don’t have time or are still uncertain, you can reach out to ForrestBrown. We will be happy to review your R&D claim and provide you with clear written advice explaining any risks and making practical recommendations for next steps.

If your claim does need to be amended to address any errors, an R&D tax adviser will know how to do this as efficiently as possible. Your accountant will typically be happy to help you as well, although they may recommend bringing in a specialist; they may even have one that they recommend.

I worked with an R&D tax adviser to prepare my R&D claim – you should share the letter with them as soon as you receive it. They should be happy to advise you and answer any questions you have.

We don’t recommend settling for a general reassurance that everything is fine. Remember that you carry the risk associated with your R&D claim, not your adviser. It is therefore your adviser’s role to ensure you understand your claim and any risks within it. If you don’t, ask questions. And if you are not satisfied with their handling of your questions, seek a second opinion. Do not wait until you receive a compliance check letter or you will have missed the opportunity to address any errors with minimal fuss.

Contact ForrestBrown for the support you need

If you have received correspondence from HMRC in relation to your R&D tax claim, it’s important not to panic and not to ignore it. You should however act quickly and decisively. It may be that you find yourself without sufficient understanding of your claim or confidence in your adviser. If this is the case then ForrestBrown can review your claim and offer the support you need on a consultancy basis.

Contact us today to find out more.